Baird Investment Banking Pitch Book

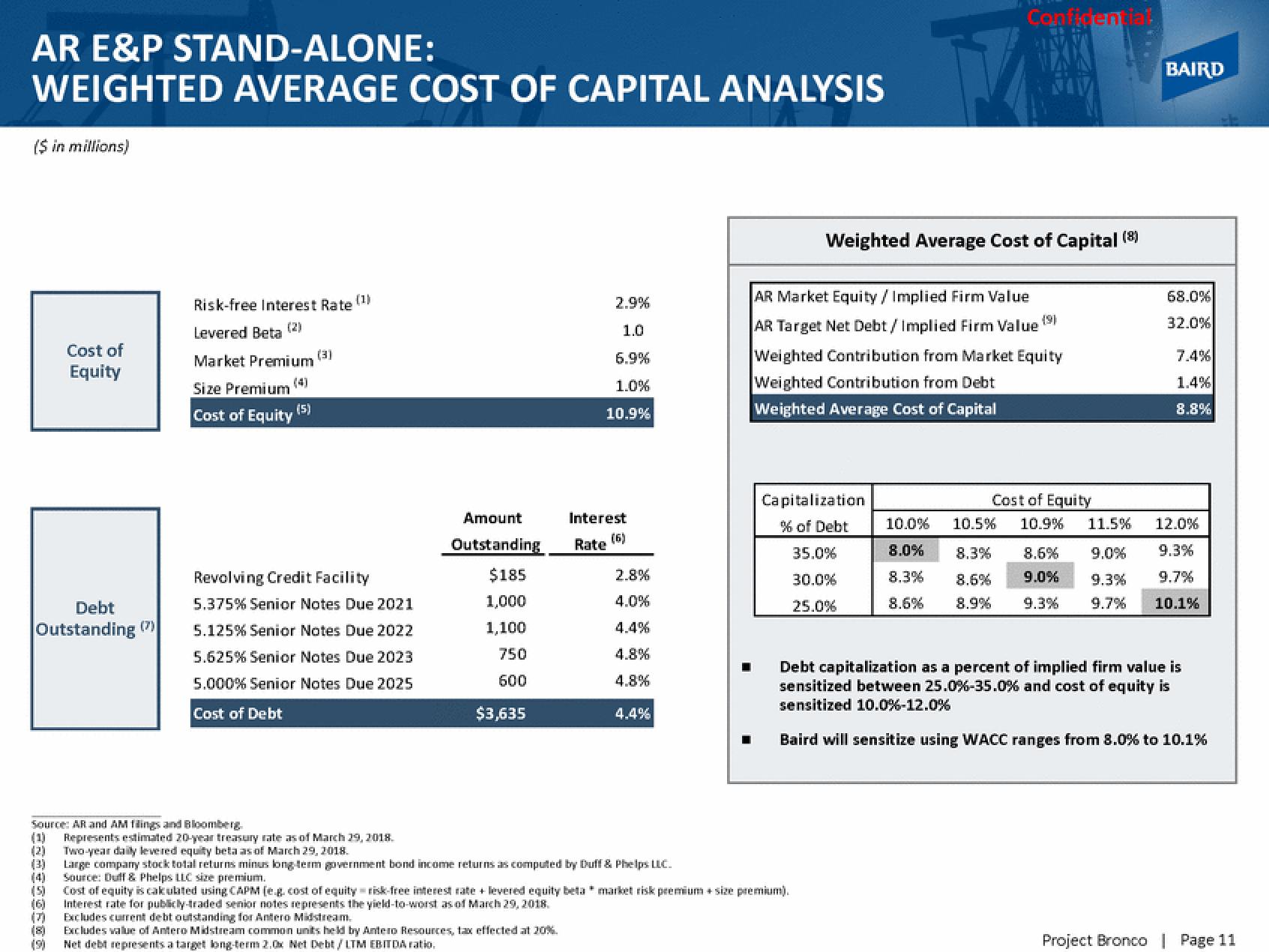

AR E&P STAND-ALONE:

WEIGHTED AVERAGE COST OF CAPITAL ANALYSIS

($ in millions)

Debt

Outstanding (7)

Cost of

Equity

(1)

(2)

(3)

(5)

(6)

(7)

(8)

(9)

Risk-free Interest Rate (¹)

(2)

Levered Beta

Market Premium

Size Premium

Cost of Equity

(5)

(3)

Source: AR and AM filings and Bloomberg

Represents estimated 20-year treasury rate as of March 29, 2018.

Two-year daily levered equity beta as of March 29, 2018.

Revolving Credit Facility

5.375% Senior Notes Due 2021

5.125% Senior Notes Due 2022

5.625% Senior Notes Due 2023

5.000% Senior Notes Due 2025

Cost of Debt

Amount

Outstanding

$185

1,000

1,100

750

600

$3,635

2.9%

1.0

6.9%

1.0%

10.9%

Interest

(6)

Rate

2.8%

4.0%

4.4%

4.8%

4.8%

4.4%

Large company stock total returns minus long-term government bond income returns as computed by Duff & Phelps LLC.

Source: Duff & Phelps LLC size premium.

Weighted Average Cost of Capital (8)

AR Market Equity / Implied Firm Value

AR Target Net Debt / Implied Firm Value

Weighted Contribution from Market Equity

Weighted Contribution from Debt

Weighted Average Cost of Capital

Capitalization

% of Debt

Cost of equity is calculated using CAPM (e.g. cost of equity risk-free interest rate + levered equity beta* market risk premium + size premium).

Interest rate for publicly-traded senior notes represents the yield-to-worst as of March 29, 2018.

Excludes current debt outstanding for Antero Midstream.

Excludes value of Antero Midstream common units held by Antero Resources, tax effected at 20%.

Net debt represents a target long-term 2.0x Net Debt/LTM EBITDA ratio,

Confidential

35.0%

30.0%

25.0%

8.3%

8.6%

8.9%

(9)

Cost of Equity

10.0% 10.5% 10.9% 11.5%

8.0%

8.3%

8.6%

BAIRD

68.0%

32.0%

7.4%

1.4%

8.8%

12.0%

8.6%

9.0%

9.3%

9.0%

9.3%

9.7%

9.3% 9.7% 10.1%

Debt capitalization as a percent of implied firm value is

sensitized between 25.0 % -35.0% and cost of equity is

sensitized 10.0% -12.0%

Baird will sensitize using WACC ranges from 8.0% to 10.1%

Project Bronco | Page 11View entire presentation